Editor's Note

This week, the cryptocurrency market endured its most destructive deleveraging process since October 2025. The global digital asset market capitalization plummeted from $2.69 trillion at the week's opening to a local low of $2.33 trillion, representing a contraction of over 13%. This violent volatility underscores a profound structural transition from a period of "valuation expansion" to one of "liquidity reshaping." Bitcoin faced multiple rounds of rigorous stress testing, flash-crashing from highs above $79,000 to test the psychological $60,000 handle before recovering toward $71,120 by Sunday's close. However, the massive liquidation of leveraged positions has fundamentally reset the short-term ownership structure of the market.

[Personal View]: The sell-off this week was not driven by a single negative event but rather a convergence of macroeconomic stressors and deteriorating micro-market structures. Macroscopically, a liquidity panic triggered by the partial U.S. government shutdown, coupled with the hawkish stance of Fed Chair nominee Kevin Warsh, significantly compressed the risk premium for speculative assets. Microscopically, on-chain data revealed that just prior to the crash, stablecoin net outflows from centralized exchanges reached multi-month peaks, indicating that institutional capital was engaging in a calculated defensive retreat ahead of peak uncertainty.

The market displayed a distinct "dual-speed" characteristic: while the secondary market suffered a brutal drawdown due to the liquidation of over $5 billion in leveraged positions , the primary market and compliant infrastructure sectors remained remarkably active. BlackRock’s IBIT spot ETF recorded a historic $10 billion in daily trading volume during the peak of the volatility, and institutional service providers like Talos and Anchorage secured massive funding rounds. This suggests that while speculative bubbles are being burst, the long-term thesis of crypto-assets as core financial infrastructure remains robust, with capital rotating from high-risk offshore speculation toward transparent, regulated channels.

Market Overview

Major crypto assets underwent significant price corrections this week. Both Bitcoin (BTC) and Ethereum (ETH) recorded weekly losses exceeding 15%, reflecting a systemic release of risk across the broader market.

Major Asset Performance (Weekly)

Data as of Feb 8, 2026, 23:59 UTC+8

Core Market Indicators

- BTC Dominance: As of Sunday, BTC dominance rebounded to 60.2%. During the liquidity crunch, capital demonstrated a classic "flight to quality," as small-cap tokens fell disproportionately more than Bitcoin, driving up BTC's relative market share.

- Crypto Fear & Greed Index: The index hit a rare low of 9 this week, the lowest level since the Terra/Luna collapse in May 2022. The week began with the index near 20, but retail sentiment entered a total breakdown as BTC broke key support levels at $74,000 and $70,000.

- Funding Rate Volatility: Long positions were decimated this week. Ethereum perpetual funding rates collapsed to -16.9% at one point, signaling an extreme bearish consensus and typical overcrowded shorting conditions.

- Liquidation Data: According to CoinGlass, total liquidations across the market exceeded $5 billion over a four-day window. On February 5, a single-day liquidation volume of $2.6 billion was recorded, primarily affecting multi-leverage longs on Hyperliquid, Bybit, and Binance.

Top Stories

- U.S. Government Reaffirms Support for Strategic Bitcoin Reserve. Treasury officials confirmed that the U.S. would maintain its strategic Bitcoin reserve and clarified that there is no intention to intervene in market pricing. This provided much-needed long-term regulatory assurance, dampening fears of large-scale government sell-offs.

- Trump Media (DJT) Sets Record Date for Digital Token Distribution. TMTG announced February 2, 2026, as the record date for shareholders to qualify for token rewards. The project, hosted via Crypto.com, marks a major milestone in integrating traditional equity ownership with digital asset incentives.

- Brazil Passes Bill to Ban Algorithmic Stablecoins. The Brazilian Science and Technology Committee approved Bill 4.308/2024, classifying unbacked algorithmic tokens as financial fraud punishable by up to eight years in prison. This regulatory pivot directly challenges the expansion of protocols like Ethena in Latin America.

- SEC and CFTC Jointly Relaunch "Project Crypto." The two major U.S. regulators released a unified rulebook to standardize digital asset classification and create shared frameworks for clearing, settlement, and custody. This marks a shift from "regulation by enforcement" to proactive collaborative framework building.

- Bitcoin Price Briefly Sips Below MicroStrategy's Cost Basis. BTC fell below the estimated institutional average of $76,037 for the first time since October 2023. While Michael Saylor reaffirmed a "no-sell" stance, secondary market concerns over institutional margin calls peaked mid-week.

- JPMorgan Maintains $266,000 Long-Term Bitcoin Target. Analysts argued that the correction below $70,000 was a necessary leverage flush, noting that Bitcoin's attractiveness to sovereign wealth funds as a hedge against fiat debasement remains undiminished.

- Swift Successfully Integrates Blockchain Ledger for 24/7 Global Settlement. The legacy financial messaging giant announced that its system now supports instant cross-border transfers via a blockchain layer, signaling that major financial institutions have moved from experimentation to industrial-scale application.

- 21Shares Files for First Spot RWA ETF with the SEC. The application, utilizing Ondo Finance's tokenized T-bill products as the underlying asset, would provide traditional investors direct access to on-chain yield, further blurring the line between DeFi and TradFi.

- BlackRock’s IBIT Records Historic $10 Billion Daily Turnover. During the crash on February 5, the record volume in IBIT suggested that large-scale asset managers were aggressively rebalancing portfolios rather than merely exiting the asset class.

- Federal Reserve Proposal for Direct Crypto Access to Payment Infrastructure Gains Momentum. A new framework would allow qualified digital asset firms to bypass commercial bank intermediaries and use the Fed’s liquidity and settlement facilities directly.

Sector Deep Dive

Real World Assets (RWA): The Institutional Safe Haven

In a week of broad market carnage, the RWA sector was one of the few to record net growth in Total Value Locked (TVL). DeFiLlama data indicates that RWA TVL has surged by $2 billion since January, exceeding $19.2 billion.

Analysis: The capital flow into RWA protocols demonstrates a "flight to quality" as crypto-native assets reached annual volatility peaks. Investors are converting idle stablecoins into interest-bearing T-bill tokens or tokenized gold, transforming RWA from a mere narrative into a vital liquidity shock absorber for the chain. However, the sector remains sensitive to U.S. monetary policy; should Kevin Warsh push for accelerated quantitative tightening, the relative yield advantage of tokenized T-bills may face repricing.

Decentralized Exchanges and Perpetual Derivatives (DEX/Perps)

DEXs served as the primary hubs for price discovery and risk management during the liquidity crisis. Weekly perpetual trading volume hit $316.6 billion, up 14.05% WoW.

Mechanism: Hyperliquid (HYPE) demonstrated extreme resilience. Despite the supply shock from its February 6 team and contributor unlock (accounting for 41.7% of BERA’s supply potential), the market had already priced in this risk through aggressive shorting. The subsequent "sell the news" event turned into a short-squeeze recovery. Furthermore, Jupiter’s integration of Polymarket signals that "prediction trading" is moving into the mainstream DEX traffic pool, providing more direct pricing signals for macro events like CPI releases.

On-Chain Highlights

- Ethereum Active Addresses Reach Record High: Despite price weakness, ETH daily active addresses exceeded 1.2 million (7-day MA), with a 30-day peak of 693,000. History suggests that a decoupling of fundamental network growth from price action often precedes a mid-term recovery.

- Bitcoin Realized Profit/Loss Ratio Nears 1: The 90-day MA of this metric is approaching the neutral 1.0 level. Falling below 1 would indicate that realized losses are exceeding profits, a condition historically associated with total market capitulation.

- Stablecoin Liquidity Contraction on Exchanges: Since November, over $4 billion in stablecoins has left centralized exchanges, with Binance alone seeing a $3.1 billion reduction. This massive withdrawal reflects extreme risk aversion and large-scale deleveraging.

- Whale Accumulation in the $60k-$65k Flash Zone: On-chain monitoring indicates that addresses holding >1,000 BTC were net buyers during the "wick" down to $60,000, while retail addresses (<$10k) were the primary source of panic selling.

- BTC MVRV Z-Score at 2023 Lows: The score has fallen to approximately 1, a level last seen in October 2023 when Bitcoin was trading at $29,000. This implies that the majority of speculative premium has been flushed out of the system.

- ETH Market Cap Below Realized Market Cap: Goldman Sachs noted that most ETH holders are currently in a loss-making position on an aggregate cost-basis. While painful, this "flushes" out profitable speculators, creating a cleaner path for future upside.

- Bitcoin Network Becomes a "Ghost Town": Analyst Willy Woo highlighted that transaction fees have hit historic lows, suggesting that speculative volume has finished liquidating and the market is awaiting a new fundamental driver.

- XRP Whale Distribution Divergence: While XRP ETFs have accumulated $1.2 billion in the U.S., large "whale" addresses (>1M XRP) have been moving positions onto exchanges, potentially to hedge against downside risk.

Funding and Project Updates

Major Funding Rounds This Week

Primary market activity exceeded $1 billion this week, focused heavily on institutional-grade infrastructure.

Key Project Milestones

- Berachain (BERA) Supply Shock Test (Feb 6): The project unlocked 41.7% of its supply. However, the Proof of Liquidity (PoL) mechanism successfully incentivized a high percentage of these tokens to be restaked, maintaining mainnet stability.

- Hyperliquid (HYPE) Largest Team Unlock: Approximately $300 million in tokens were released to core contributors. HYPE's strong fundamental role in current derivatives pricing allowed it to be one of the few tokens to trade higher on the week.

- DJT Token Distribution Standards: Crypto.com confirmed the use of multi-sig cold storage for shareholder tokens, establishing a new standard for transparency in equity-token crossovers.

- Ethena (USDe) Contraction: In response to the Brazil ban news, USDe circulating supply dropped by 8% as users moved to more regulated stablecoin alternatives.

- Optimism (OP) Buyback Plan: The governance committee approved a milestone proposal to use 50% of revenue for token buybacks starting this month, injecting a long-term deflationary narrative into the OP ecosystem.

Regulation and Macro

Regional Focus

- United States: The nomination of Kevin Warsh as Fed Chair suggests a potential hawkish pivot in 2026, with markets pricing in faster quantitative tightening. This has applied downward pressure on non-yielding assets like Bitcoin. Conversely, the SEC's guidance on "Tokenized Securities" provided legal clarity for the RWA sector, confirming the validity of on-chain ownership transfers.

- European Union: A split in regulatory execution is emerging. While MiCA is in effect, 12 member states missed the DAC8 tax rule deadline, raising concerns about internal regulatory arbitrage within the bloc.

- Asia: Hong Kong's SFC concluded consultations on crypto dealers and custodians, with legislative proposals set for early 2026 to integrate these providers into the formalized securities framework, likely attracting new family office capital.

Spot ETF Net Flows (Feb 2–06)

Sentiment in the spot ETF market shifted dramatically from "Greed" to "Risk Management."

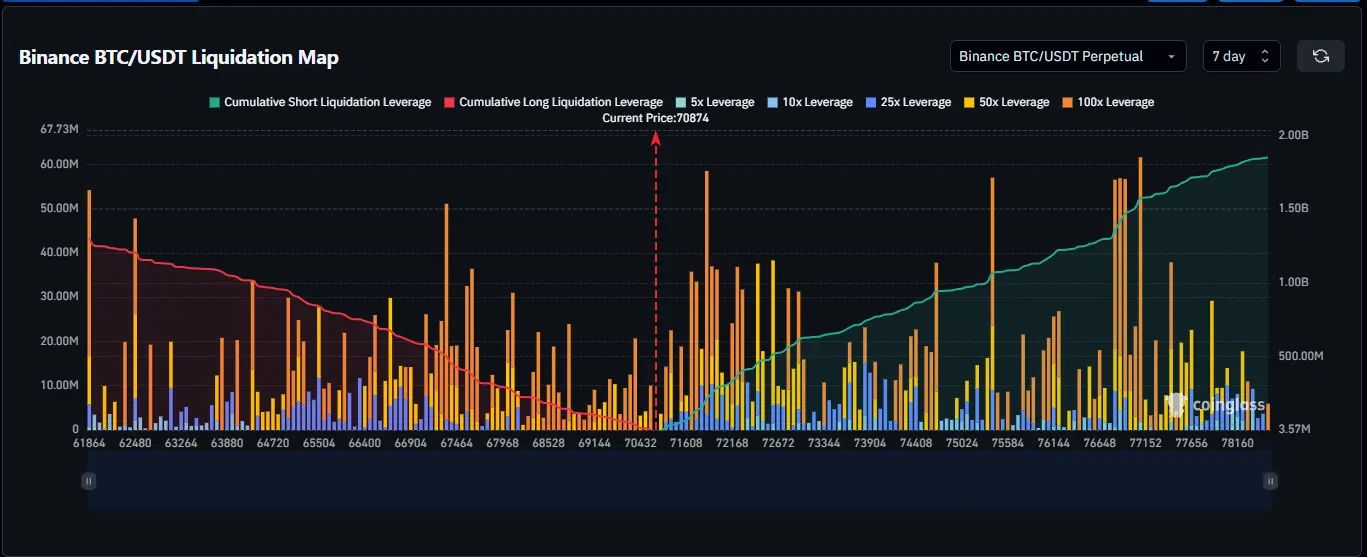

Chart of the Week

1. BTC Liquidation Heatmap

The heatmap for this week reveals a total wipeout of nearly $800 million in long leverage that had accumulated above $73,000. Liquidity has now shifted to the $75,000+ zone where a massive cluster of short liquidations is building.

Next Week to Watch

- U.S. January CPI (Feb 11): Expected to show a cooling trend. A downside surprise could revive June rate-cut hopes, acting as a massive tailwind for Bitcoin.

- U.S. January PPI (Feb 12): Crucial leading indicator for inflation and the Dollar Index's short-term trajectory.

- CME ADA/LINK/XLM Futures Launch (Feb 9): CME officially enters these asset classes. Watch for high initial volatility followed by a gradual increase in institutional participation.

- MegaETH Public Testnet (Feb 9): Performance data from this launch will determine the valuation anchors for the high-performance L2 sector in 2026.

- U.S. Delayed Employment Report (Feb 11): Data delayed by the shutdown will provide an asymmetric volatility risk to macro markets.

- Robinhood 2025 Annual Results (Feb 10): A key window into retail sentiment and the health of the 2025 crypto rally.

- Berachain (BERA) Post-Unlock Price Floor: Markets will monitor if the 41.7% supply injection finds a stable accumulation zone by mid-week.

- SENT AI Final Mainnet Roadmap: Expected release of technical milestones ahead of its Feb 25 launch.

Closing & CTA

The extreme volatility of the past week is a stark reminder that even in an institutional era, the crypto market remains prone to rapid deleveraging. Bitcoin’s successful defense of the $60,000 level and the record volume in managed ETFs suggest a more resilient market foundation than in previous cycles. Do not let the "Red Candles" obscure the long-term logic: the most significant opportunities are often found during the "Extreme Fear" phases of the cycle.

Thanks for reading AscendEX Web3 Weekly

Subscribe for weekly delivery: https://ascendex.com/en/digest

Trade Bitcoin and 800+ cryptocurrencies: https://ascendex.com

This report is for informational purposes only and does not constitute investment advice. Cryptocurrency prices are highly volatile. Invest responsibly. AscendEX assumes no liability for the content of this report.